Definition of monopoly market

A monopoly market refers to a market situation in which only one commodity seller exists. A monopoly market refers to a market structure in which a single producer or seller controls the entire market. This single seller deals in products that have no close substitutes. Some of the definitions of monopoly given by different economists are as follows:

Prof. Thomas: “Broadly, “At a broad level, the term ‘monopoly’ encompasses the concept of wielding effective control over prices, whether in terms of supply or demand for goods and services. More specifically, it refers to the collaboration of manufacturers or merchants allying to manipulate the supply price of commodities or services.”

Bilas: “A state of pure monopoly is defined within a market scenario where a solitary seller exclusively offers a product without any viable substitutes. This lone seller operates independently, uninfluenced by, and non-influential to the prices and outputs of other products circulating in the broader economy.”

A.J. Braff: “Under pure monopoly, there is a single seller in the market. The monopolist demand is market demand. The monopolist is a price market. Pure monopoly suggests no substitute situation.”

Thus, as a single seller, a monopolist may be a king without a crown. If there is to be a monopoly, the cross-elasticity of demand between the product of the monopolist and the product of any other seller must be very small. There is only one supplier in the market but many demanders, so many that no buyer has any control over the prices.

In the landscape of a monopolized market, the defining elements are the barriers to entry, presenting as restrictions that impede the ingress of new firms into a specific industry. These barriers act as formidable hurdles, shaping the competitive dynamics and fortifying the monopolistic nature of the market. Because of barriers, new firms cannot profitably enter that market. A monopoly is a market structure in which one firm makes up the entire market. It is the polar opposite of competition. It is a market structure in which the firm faces competitive pressure from other firms.

Features of Monopoly

A monopoly exists when a single seller controls the supply of a good or service and largely determines its price. The major characteristics define a monopoly.

One seller and a large number of buyers: The monopolist’s firm is the only firm; it is an industry. But the number of buyers is assumed to be larger.

No substitutes: There are no close substitutes for the goods or services that the monopoly sells. Thus, the cross elasticity of demand between the product of the monopolist and others must be negligible or zero.

Barriers to entry: The monopolist is protected by obstacles to competition that prevent others from entering the market.

Almost complete control of market price: By controlling the available supply, the monopolist can control the market price. Every monopolist itself is a price maker.

Price discrimination: When a monopoly firm charges different prices from different customers for the same product it is called price discrimination. Its aim is profit maximization.

Non-price competition: The product produced by a monopolist may be either standardized or differentiated. Monopolies dealing with standardized products often focus on public relations advertising as their primary marketing strategy. In contrast, monopolists offering differentiated products may choose to highlight and promote specific attributes of their products through advertising campaigns.

Profit in the long run: In the long run, a monopolist has the opportunity to secure extraordinary profits, as the absence of competitive sellers eliminates the concern of market rivalry. This unique market position empowers the monopolist to sustain abnormal profits without the pressure of competition.

Losses in the short run: Generally, a common man thinks that a monopoly firm cannot incur a loss because it can fix any price it wants. However, this understanding is not correct. A monopoly firm can sustain losses equal to fixed costs in a short period.

Comparison of Perfect competition and monopoly

Each row highlights differences in various characteristics of the two market structures.

| Characteristics | Perfect Competition | Monopoly |

|---|---|---|

| Number of firms/sellers/products | Many | One |

| Type of product/service sold | Indentical | Good and service with not close substitutes |

| Barriers to entry | None: free entry and exit | yes: high |

| Price-maker-no competitors; no close substitutes | Price taker; price given by the market | Price-maker-no competitors; no close subsitutes |

| Price | P=MR=MC | Set, P>MR=MC |

| The demand curve facing the firm | Horizontally sloped; perfectly elastic demand curve | Downward-sloping |

| Social surplus | Maximized | Not maximized, but sometimes benefits from research and development |

| Equilibrium long run profits | Zero: Normal profit | Potentially greater than zero |

Price and Output Determination of Firm and Industry under Monopoly Market

Short-Run Equilibrium

In the short run, the monopolist should make sure that the price does not go below average variable cost (AVC). The equilibrium under monopoly in the long run is the same as in the short run. In the extended perspective, the monopolistic entity possesses the ability to scale up its production facilities in response to market demand. This strategic adaptation aims to align marginal revenue (MR) with the long-run marginal cost (MC).

For a firm in perfect competition, marginal revenue always equals price. This is because firms in perfect competition are, by assumption, price takers. Monopolists, by contrast, are not price takers. Consequently, the price does not equal the marginal revenue for monopolists. A monopolist, similar to a firm in perfect competition, will keep producing more goods as long as its marginal revenue is greater than its marginal cost. Marginal revenue is what we get if we sell another good. Marginal cost is what we sell as an additional good.

- If Marginal revenue > Marginal cost, the firm increases its profit by producing more.

- If Marginal revenue < Marginal cost, the firm increases its profit by producing less.

In the short run, the monopolist will maximize profit or minimize loss by producing the output at which marginal revenue equals marginal cost. In the short run, monopolists can earn excess profit, normal profit, or loss. It is determined by the price (AR) and average cost (AC) as illustrated in the following table.

| Condition | In Words | Outcome |

|---|---|---|

| AR > AC | The average revenue is greater than the average cost of production. | The monopolist makes an abnormal profit. |

| AR = AC | The average revenue is equal to the average cost of production. | The firm makes normal profit. |

| AR < AC | The average total cost of production is greater than the average revenue. | The firm makes losses or the firm will operate to minimize loss. |

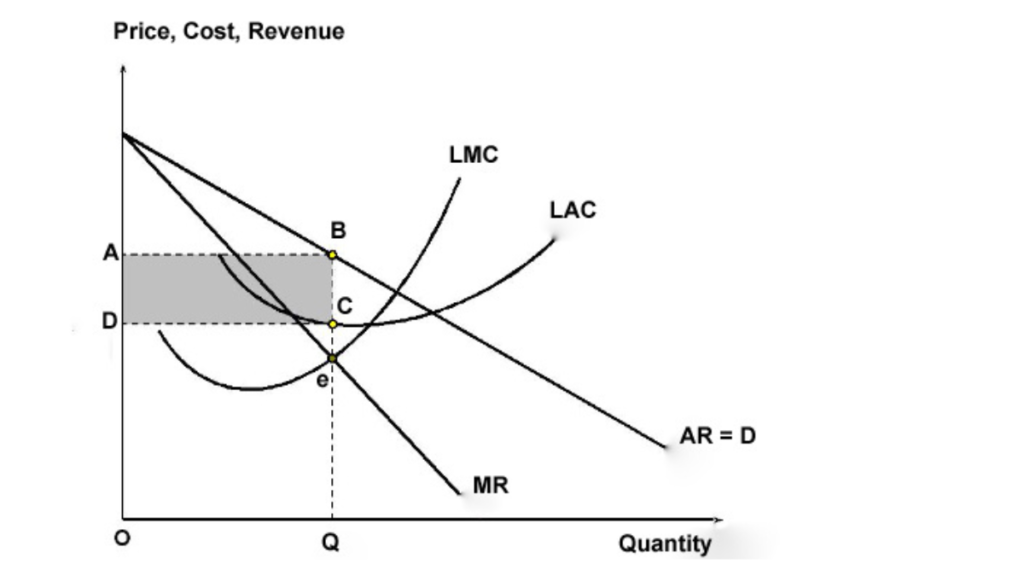

Long-Run Equilibrium

In perfect competition, economic profits are impossible in the long run. The entry of new firms into the industry drives the product’s price down until profits reach zero. Extremely high barriers to entry, however, protect a monopolist. In the long run, the monopolist has great flexibility.

The monopolist can alter its plant size to lower costs just as a perfectly competitive firm does. Facing long-run losses, the monopolist will transfer its resources to a more profitable industry. Since the monopolist does not face the threat of entry of new firms, it is not necessary for him to reach an optimal scale. Thus, a monopolist will not stay in business if he makes losses in the long run. For the long-run equilibrium,

- MR = LMC

- LMC cuts the MR from below.

Under these conditions, the price and output determined in the long run under monopoly can be explained with the help of the following diagram.

1 thought on “Monopoly Market”